10 Most Common Product Manager Mistakes, The Neobank Strategy Playbook, and a16z Fintech Predictions

We will go through the most common PM Mistakes, decode the Neobank strategies, and check what a16z partners predict for Fintech in 2024

Thank you very much for walking this path with me!

Linkedin Performance

Edu's Newsletter & Posts performance

Start date: April 22nd, 2023, mapping the 2023 Fintech Trends

Newsletter editions: 12, averaging 1 newsletter every 3 weeks

Subscribers: 1,689

Impressions: 842,323 —> almost 1 million! 🤯

Followers: 7,799

2024 Goals

Get help to keep cadence

Scale Substack

Post 1 newsletter edition/week

Post 3 relevant posts/week

Monetize

🥰I cannot thank you enough for the support I've received. Writing has not only helped me learn and level up my skills but also found great joy in sharing with others. The support I receive from you helps me keep pushing and investing time on my weekends or late hours to keep it up.

10 Most Common Product Manager Mistakes 😱

I've made many mistakes during my PM career, interviewed hundreds of PM candidates, and worked with dozens of other PMs. Some common mistakes are repeated over and over again in the Product Practice. Here are my top picks:

Let's do it all PM: this is one of the most dangerous species of Product Managers. This PM will not only fail at prioritizing what is most important but also burn the team in the process. Expect delays and poor outcomes.

Lack of vision and strategy: focusing too much on the short term without a clear vision or strategy for the mid and long term.

Output-oriented, not outcome-oriented: this is the feature factory PM. The situation is even worse when there is no objective at all, just shipping features. Prioritizing "shipping features" vs "increasing retention by XYZ, increasing contribution margin by ABC, etc.", or a tangible metric can result in a feature factory team.

Not analyzing metrics nor iterating post-release: this generally goes hand in hand with the above. The most common mistake here is to ship features and never go back to look at results or iterate to get better outcomes.

Not understanding the users' problems: too much focus on solutions, execution mode all the time, and copy-pasting the competition without ever interviewing customers, collecting feedback, or understanding what they need.

Too much focus on research vs execution: Customer interviews can give you 50% of the answer, but they are meant to be guiding data points, not blockers for execution. A good combination of execution, and fast iteration, blended with primary research can build the best products

Poor prioritization: not having good frameworks to prioritize products, and just shipping whatever comes to mind or the strongest voice in the room screams. Whatever you build needs to have some backup of impact expected, effort needed, confidence users need it and solves a real pain, and alignment with an overall long-term strategy. It needs to strengthen your core or help differentiate yourself from the competition.

Weak product requirements definitions: one of the biggest hindrances of a team's velocity is poor product definition. This causes tons of re-work, and doubts, and slows the team down.

Lack of dependency mapping: larger-sized products and features can have dependencies with other teams such as fraud, Ops, or Finance, among others. Failing to identify those dependencies from the beginning can delay development or even shut down the feature.

Not aligning with stakeholders: product managers need to communicate and align with all stakeholders across the organization. Lack of doing so can cause misalignment of what is important, can make PMs miss big risks related to their product and features, and affect overall outcomes and customer experience.

These are some of the mistakes and most common mistakes I've gone through throughout my career. I am sure there are plenty more, if you think of any others please leave a comment below!

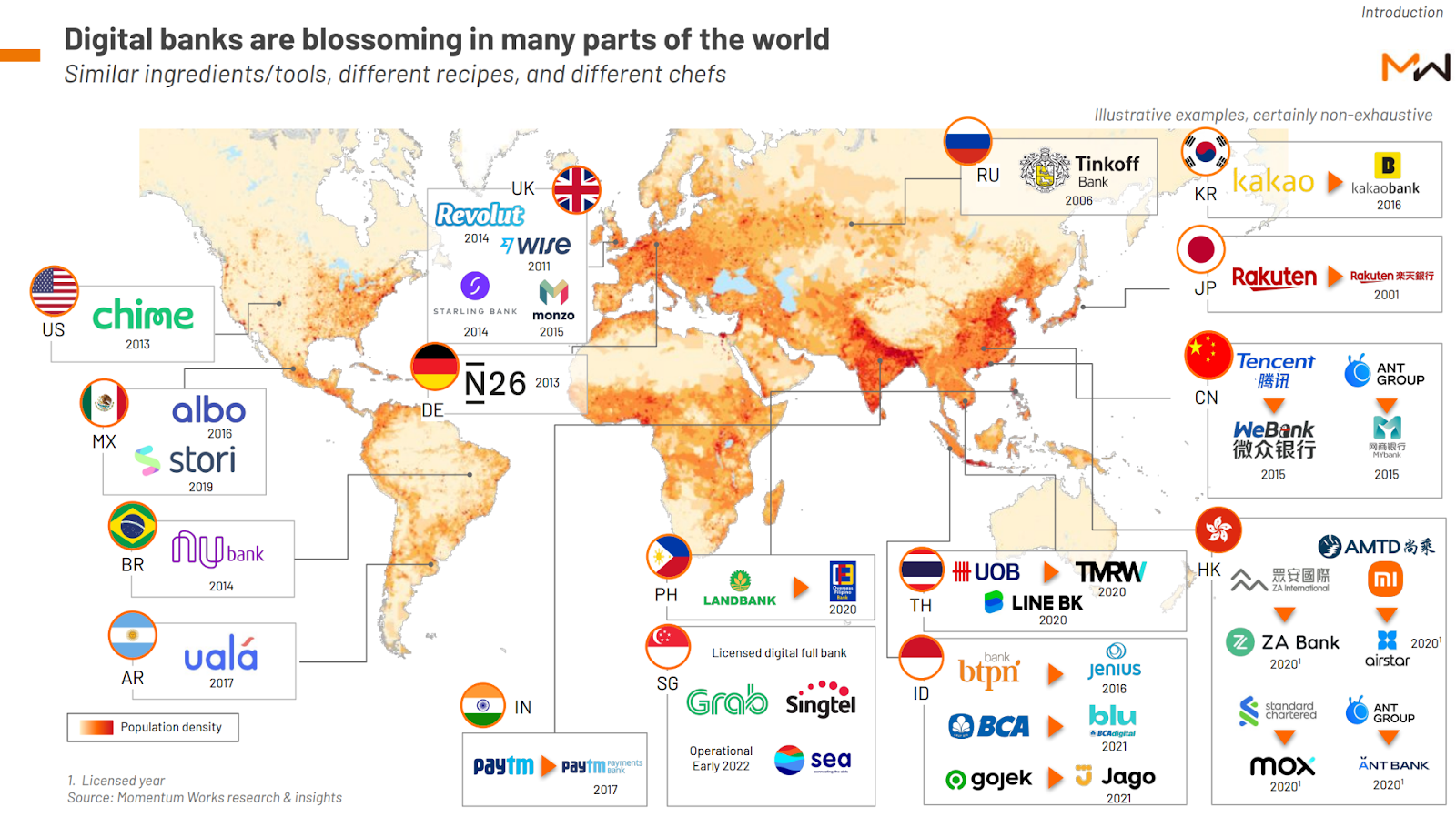

The Neobank Playbook 📖

Digital banks have exploded over the past years, following a similar playbook:

More flexible cost structure + more customer data points =

expanded customer base, better customer experience, and better margins

Trends that accelerated adoption over the past years

Everybody going Fintech using their customer base as distribution channels: Big tech Cos, such as Apple, MercadoLibre, and others, are using their flexible cost structure, large customer base as distribution channels, and direct customer touchpoints to cross-sell financial services among others

BaaS providers and competition-friendly regulation have allowed new players to compete in the financial services industry: building a wallet or credit card product in the B2C space in Latin America has become significantly easier than in the past. With BaaS providing these services via plug-and-play APIs, and Central banks being more flexible, you can now ship a fintech in a few months.

The pandemic accelerated financial inclusion: e-commerce, mobile, and digital payments exploded during the pandemic. The payment habit is expected to stay for the long run, and many players have taken the chance to position themselves as the preferred financial institution during these times.

Old, but mostly accurate, this needs to be updated to 2023.

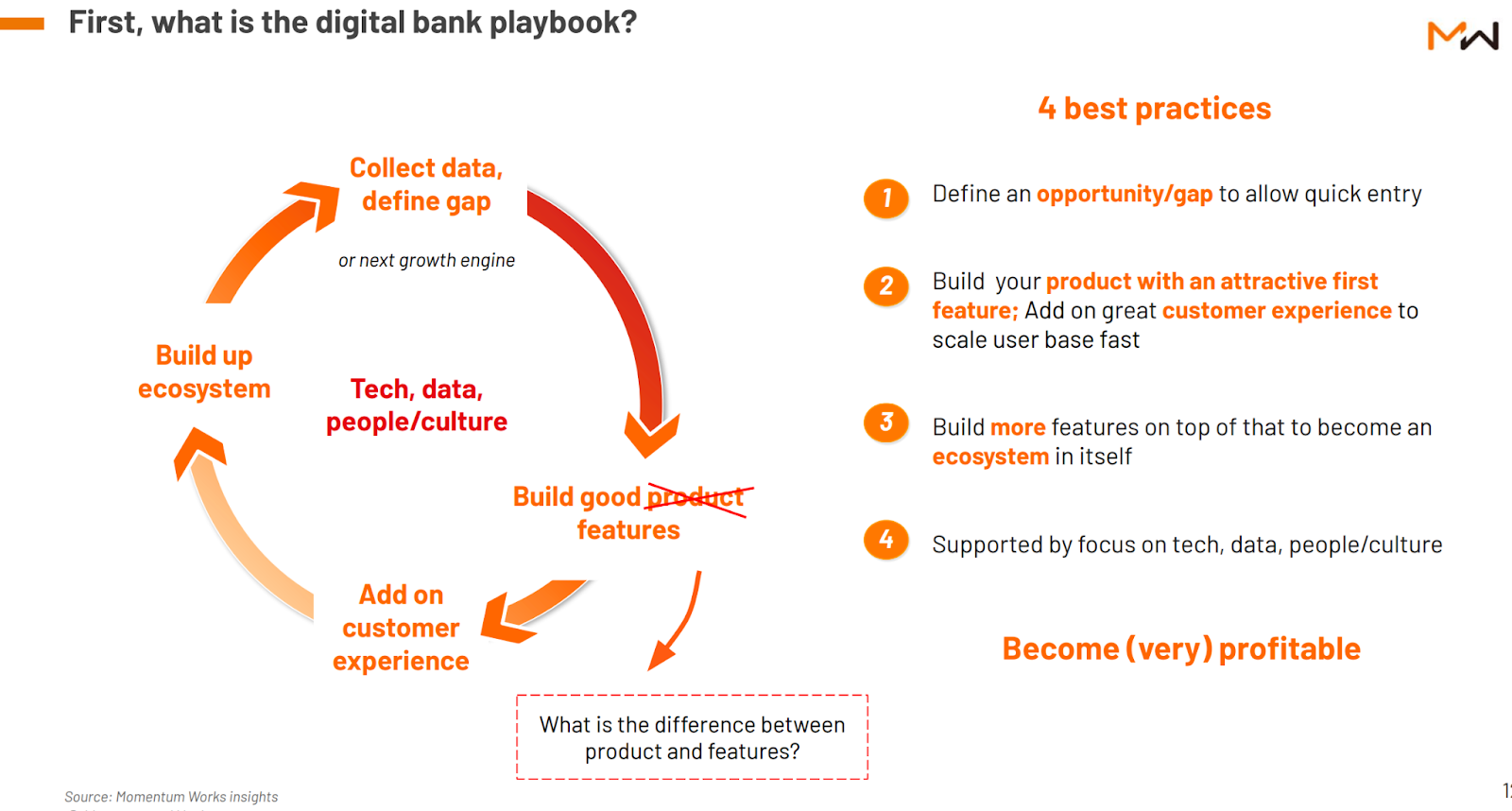

The 4-step Digital Bank Playbook

Identify which part of the customer journey to attack within the financial services industry that is underserved or poorly served and which customer segment to focus on

Build your first product with a differentiating feature and great UX/UI

Expand your ecosystem, without losing the focus on your core

Invest in platformization and focus on tech, data, people, and culture

Become profitable

In the current dry-money VC ecosystem, profitability plays a strategic role in survival. The common Fintech practice of burning money to attract customers over the past years is no longer feasible.

Today to win the game you need to build differentiative, sticky products and features customers love.

And have the stomach, time, and resources to keep the lights on until you get there.

Playbook in detail with examples below:

Big Ideas in Fintech in 2024 by a16z 💡

💼 Rise of Developers as Buyers: Developers are becoming increasingly influential in the purchase of financial services infrastructure. Fintech companies are focusing on providing a great developer experience, offering sandboxes for testing, and open-sourcing parts of their solutions to cater to this developer-centric trend. Even larger financial institutions are recognizing the importance of appealing to developers in their buying decisions. – Angela Strange, a16z fintech general partner

🏦 Tech Helps Community and Regional Banks Compete: Community and regional banks are under pressure due to regulatory changes and margin compression. Fintech companies are expected to step in and provide tools and technology to help these banks compete with larger institutions, manage risks, and better serve their clients. – David Haber, a16z fintech general partner

🤖 Financial Professional Services Get Supercharged by Software: The professional services sector within financial services, including accountants, tax advisers, wealth managers, and investment bankers, will see significant changes. Generative AI and LLMs will enable automation of tasks such as data collection, research, summarization, and report generation. Human professionals will focus on specialized expertise, reviewing automated work, and engaging with clients. – Seema Amble, a16z fintech partner

📊 LLMs Capture New “Foundational Customer Units”: Startups leveraging Large Language Models (LLMs) will capture previously challenging unstructured data, automatically tagging and storing it. This data capture could disrupt segments of the market traditionally served by software oligopolies, particularly in areas where data ingestion was limited. – Joe Schmidt, a16z fintech partner

🚀 Innovation in Banking and Trading Tools: Fintech founders are expected to address longstanding challenges within financial institutions, particularly in investment banking and trading services. Many of the tools used in these sectors are outdated or manual, creating opportunities for new solutions. Banks are increasingly willing to adopt new tools, which may lead to innovation in these areas. – Marc Andrusko, a16z fintech partner

🤖 AI Will Push Latin American SMBs to Go Digital: Latin American small and medium-sized businesses (SMBs) are expected to increasingly adopt AI assistants for customer service and support, streamlining tasks and improving response times. However, structural challenges, such as the prevalence of pen-and-paper operations, remain obstacles that startups can help address. – Gabriel Vasquez, a16z fintech partner

💰 AI Will Be the Key to Higher Return on Equity (ROE): Financial institutions are set to adopt AI-native applications across various operational workflows. This adoption will likely have a significant economic impact on their profit and loss (P&L) statements. Use cases will span revenue generation and middle- to back-office functions, with a focus on engineering, procurement, legal, compliance, and risk management. – David Haber and Marc Andrusko

All these trends reflect the evolving landscape of fintech in 2024, with a strong emphasis on technology-driven innovation, automation, and the growing influence of developers in financial services decision-making.

That was all, see you next year!

Thank you for reading my newsletter, happy new year!!!

If you enjoyed it, please subscribe with the link below and share it with your friends and colleagues.

Un abrazo,

Edu